Market update: Off to the races

With a gain of more than 2%, the S&P 500 is headed into the weekend firmly above 4,000 for the first time since mid-December. The breadth of the rally was wide, with nearly 400 stocks in the green on the week. The tech-laden NADSAQ 100 outperformed, with its +4% rise pushing it above its 200-moving average for the first time since March 2022.

That said, stocks don’t have an all clear signal yet. Only one quarter of the S&P 500 has reported Q4 2022 earnings. The takeaway so far: A mixed bag, but better than feared. For one, J&J beat earnings, despite a slowdown in revenue and sales in the face of a strong dollar and diminishing COVID-19 vaccine demand. Microsoft’s Azure cloud business persists as its engine of growth, but the company seems poised to guide expectations lower from here. Looking ahead, many of the “big name” announcements are still to come, including the likes of Google, Apple and Amazon next week.

In the bond market, Treasury yields did a round-trip as economic data showed bits of both strength and weakness. On one hand, preliminary U.S. Manufacturing and Services PMIs for January continued to point towards contraction. On the other, filings for unemployment benefits hit their lowest level since early last year. This leaves investors wondering when, and if, the next shoe will drop.

Elsewhere, the U.S. government is still grappling over what to do with the debt ceiling, and other big macro catalysts, such as the February FOMC meeting and January nonfarm payrolls, are on deck for next week.

In the meantime, here are five quick observations worth paying attention to.

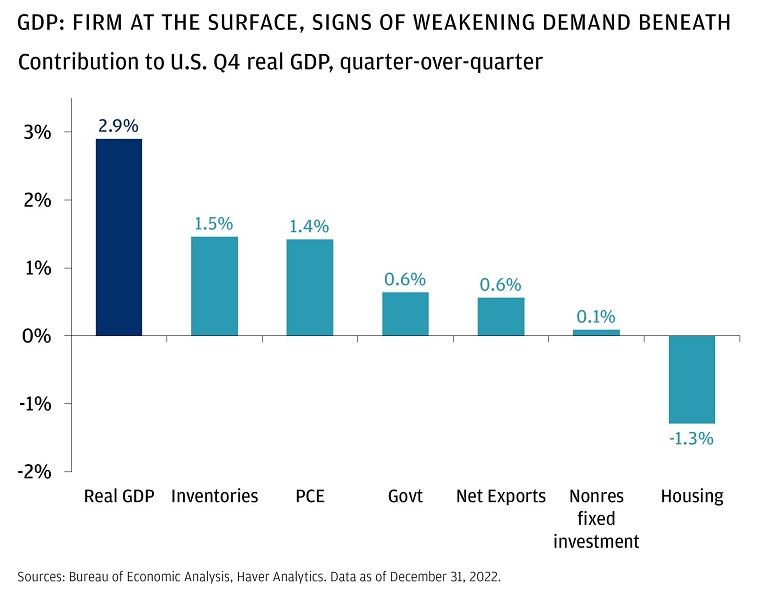

1. The U.S. economy: Strong (at first glance), but losing steam. The latest GDP data showed that the U.S. economy grew at a +2.9% real (inflation-adjusted) pace through the final quarter of 2022. The headline number implies strength, but digging into the details reveals less favorable dynamics. There were three components that caught our attention: 1) Inventories, which continued to build as goods demand weakened, contributing about half of the growth reported, 2) consumption, which came in still-solid, but slower than expected, and 3) capex (offering a pulse check on corporate America), which appears to be cooling despite firm spending on tech. In all, the report suggests that while the U.S. economy grew at the end of last year, it appears to be losing momentum.

2. The bond market: A record start. Bloomberg’s global bond index has surged over +3% in 2023, the best start to a year in over two decades. The prospect of the end of the global tightening cycle is prompting borrowers to seek opportunities to raise financing and making investors finally ready to take on debt. Global issuance of investment- and speculative-grade government and corporate bonds across currencies reached near $600 billion year-to-date (through Jan. 18), the biggest tally on record for the period.

Take Caesars Entertainment (stock +27% year-to-date), which offered over $3 billion in bonds and leveraged loans earlier this week, one of the biggest refinancing deals in both markets this year. Investors jumping on “risky” debt issuance gives companies like Caesars a little longer runway, but it’s unclear what the Fed thinks about the recent easing of financial conditions. We still prefer to stay in the high quality parts of the market, given we expect spreads for riskier bonds to widen meaningfully from here in the event of a recession.

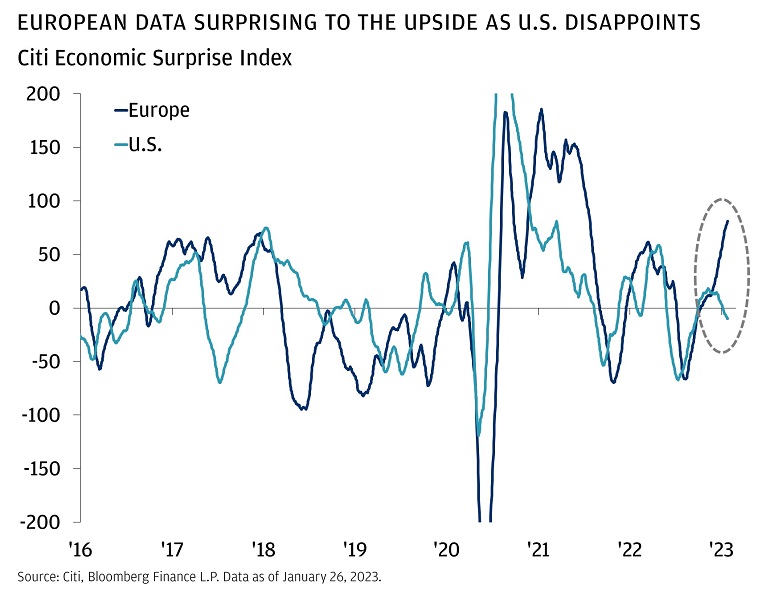

3. European equities: First inflows in nearly a year. While the sum of inflows was only $200 million last week, it’s a significant turnaround from near-record outflows just one year ago. The catalyst: The worst case economic scenario for the region seems to have faded over the past few months. A warmer-than-feared winter has left natural gas supplies near ~75% of storage capacity, relative to the ~55% typically seen at this time of the season. The strength in activity data (most recently, January Eurozone composite PMIs unexpectedly entered expansionary territory for the first time since last summer) combined with easing inflationary pressures from dramatically lower energy prices has led to a +20% equity rally (in local currency terms) from late last year’s lows. For U.S. dollar investors reaping the tailwind of a weaker USD, it’s an even higher 30%. Looking ahead, investors may look at the still-wide valuation discounts (~25% relative to the U.S.), brighter economic growth prospects, and a peaking dollar as reasons to keep adding to ex-U.S. exposure.

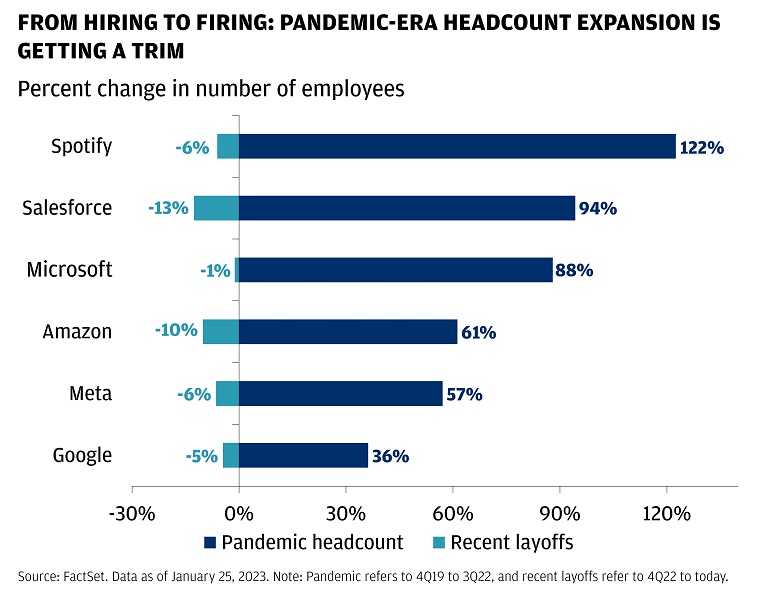

4. Corporate layoffs: The list is growing, yet the stocks are among the best performers this year. The latest tally of layoffs (which now include many of the mega cap tech names) reveal that the companies are persistently contained within tech, finance and real estate – the most interest-rate sensitive sectors of the economy. Notably, so far this year, these sectors in the S&P 500 are also at the top of the returns leader board. Communication services (+13.4%), tech (+9.4%), and real estate (+8.2%) are outperforming the broader index (+5.6%) with financials (+5.8%) nearly in-line. Broad weakness across industries has yet to reveal itself (as we expect in our base case scenario by year-end), yet these dynamics keep the sought-after soft landing window open.

5. Housing: Finding a footing. Following a record string of declines over the past two years, sales of new homes in the U.S. rose for a third consecutive month in December. Housing starts for single-family homes also saw their first gain in four months. The 1% fall in mortgage rates catalyzed the largest weekly jump in mortgage applications since 2020. While it’s hard to tell a story or predict a path forward from early-days data points, signs are pointing towards a sense of stability in what has been the most beaten up segment of the economy over the past year.

The equity market is also paying attention to the green shoots. S&P Homebuilders, which includes businesses from appliance stores to, the obvious, home building materials sellers, bottomed in June of last year and is now up near +30% from lows (with over a third of the rally coming just over the past few weeks). While housing market conditions are merely inflecting, the equity market is starting to feel comfortable with the direction of travel.

The remaining question lies in how the Fed is feeling about, by one metric, the loosest financial conditions we’ve seen since early last year. The shift in sentiment is re-activating capital markets, but early optimism may be a concern in the midst of still-elevated inflation. At the February FOMC meeting, we expect Chair Powell to hike the policy rate by 25bps and remain on the front foot with hawkish rhetoric.

Although the end of the tightening cycle is likely near, we also believe that we’re not yet out of the woods. Investors have historically been rewarded for sticking with their long-term plan, and considering opportunities that fit within their risk profile – amongst the opportunities we think are worth considering today are core fixed income, preferreds, small- and mid-cap equities, and more specific dislocated segments such as semiconductors.

As always, your J.P. Morgan team is here to discuss these insights with respect to your portfolio.