Columbia Threadneedle: Gain Clarity In 2022

Taking an active approach in fixed income will be key to finding investment success in the upcoming year.

In 2022, we expect the market narrative to transition to the traditional expansionary phase of the business cycle. Here’s what it means for fixed-income investors.

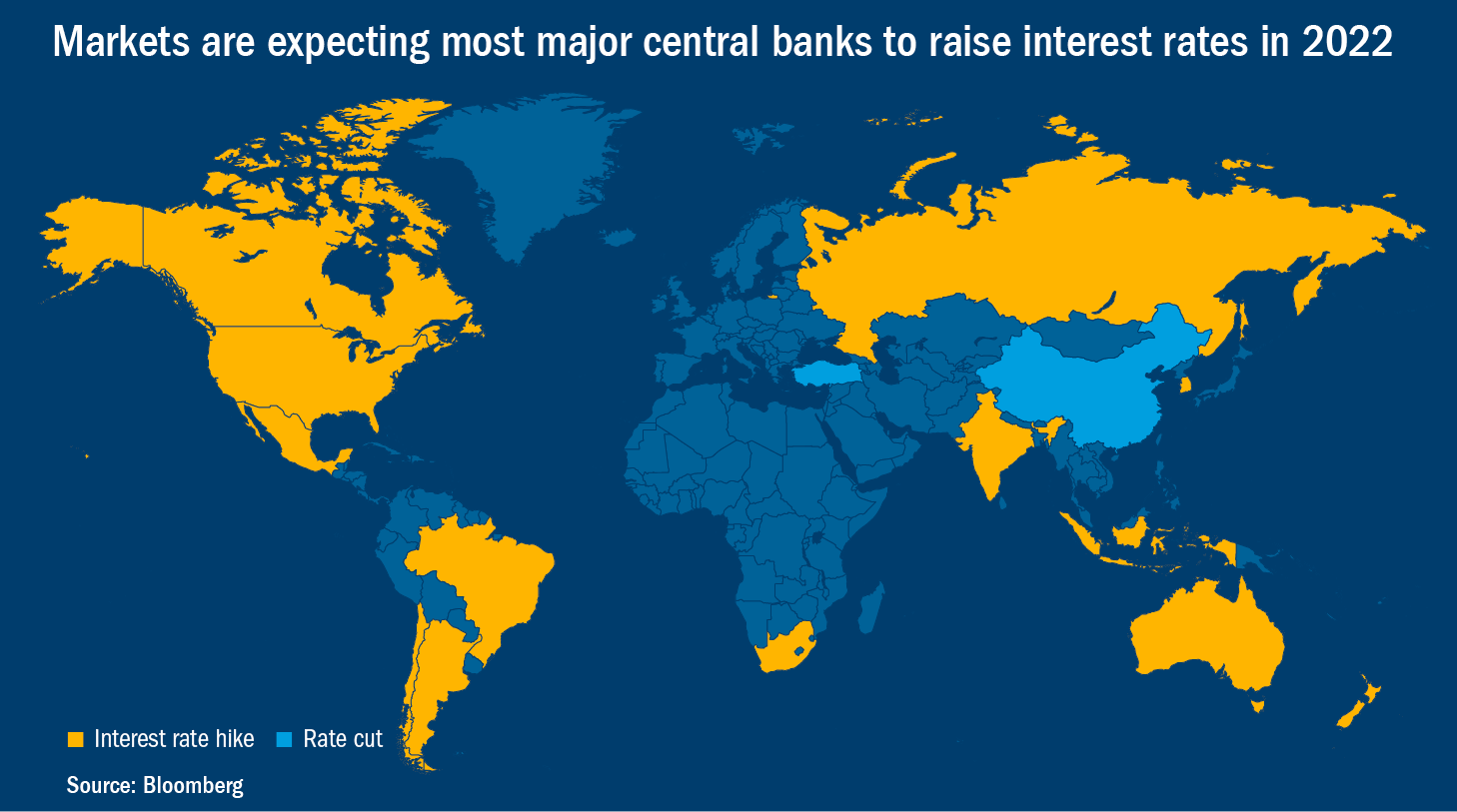

Monetary headwinds

Throughout 2021, the invisible hand of easy global monetary policy supported financial markets. But for 2022, the outlook is quite different. We’ve already seen central banks pare asset purchases, and we should expect a very different backdrop for short-term interest rates, pricing in rate hikes for most major central banks. This waning monetary support coupled with expensive starting valuations warrants a more selective approach to fixed income in 2022.

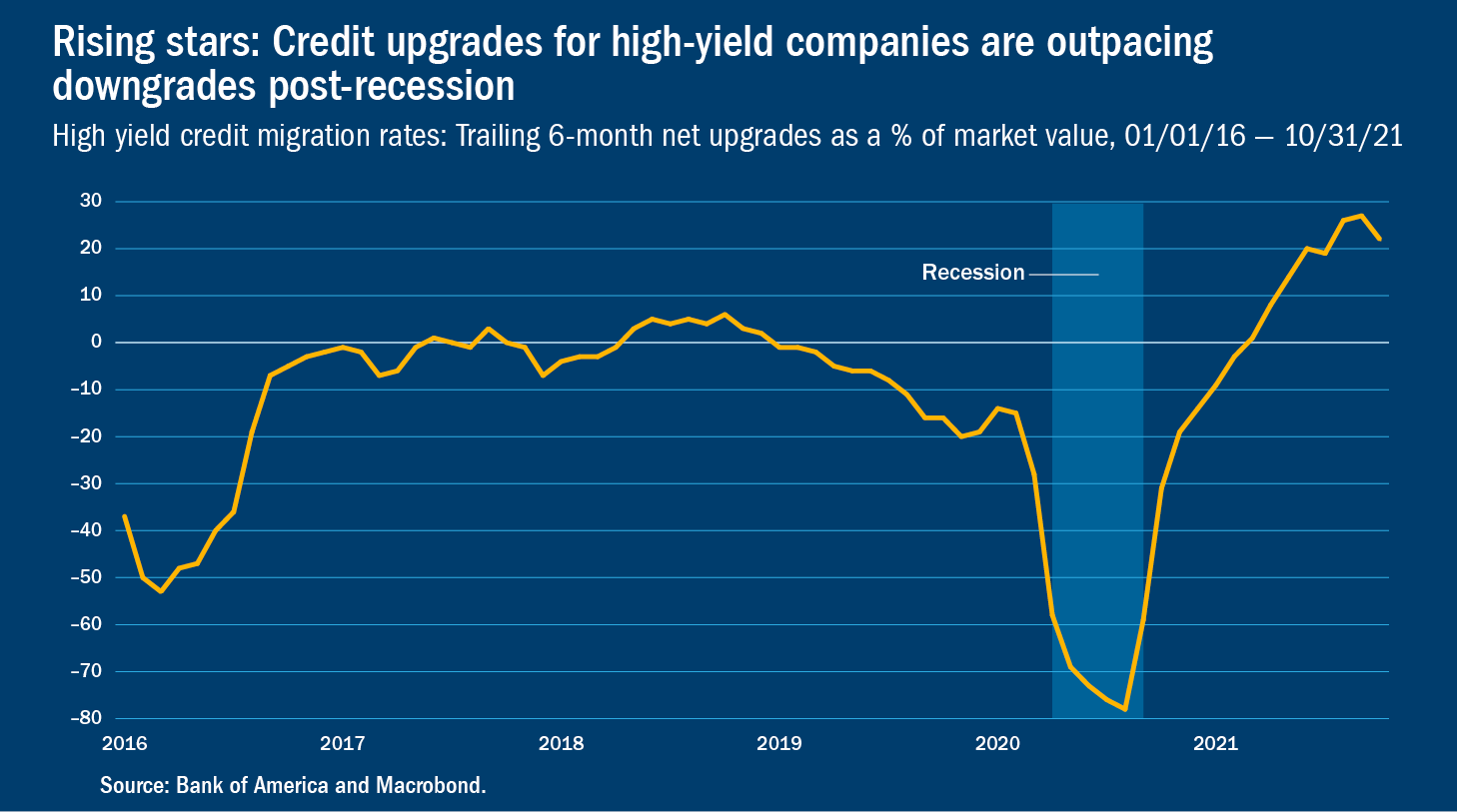

Star potential

During recessions, it’s common for rating agencies to downgrade companies whose economic fortunes start to dim. The volume of these “fallen angels” during the pandemic was historic — $184 billion of corporate debt lost its investment-grade status. Aggressive management of costs, capital expenditures, dividends, share buybacks and capital structures all helped stabilize corporate cash balances. As demand steadily returned, profit margins and free cash flow grew rapidly, allowing companies to pay down debt and improve credit quality. We believe 2022 will be a strong year for “rising stars” as many high-yield companies achieve investment-grade status.In an environment where price appreciation appears muted, rising star candidates could represent a rare opportunity for gains. Risk premiums between BB- and BBB-rated bonds still offer value and prices could rise as investors anticipate higher ratings. But it takes targeted fundamental credit research to identify these favorable credit stories ahead of ratings agency action.

Off benchmark benefits

The COVID-induced liquidity wave pushed investors back into financial markets globally and drove valuations to historically expensive levels across most liquid bond markets. The notable exceptions are bonds that are less liquid, less followed or less benchmarked. This is particularly true in structured credit and municipal bonds. Nearly 40% of mortgage- and asset-backed securities are not included in any benchmark, including most of the higher-yielding opportunities in that universe. The same dynamic occurs in the municipal bond space, where a high degree of fragmentation, small issue sizes and frequent absence of credit ratings mean that muni benchmarks don’t include a lot of the opportunity set. In each case, a research-driven active strategy can flesh out the risk/return tradeoff in these areas to pursue higher income and return prospects than passive alternatives.

Get smart

Traditional passive approaches track market cap-weighted indices that are concentrated in the most indebted issuers. In today’s environment, that results in disproportionately high exposure to low-yielding government debt and corporations with bloated debt loads. An alternative, low-cost solution is a “smart beta” fixed income approach. Informed by the experience of active management, these cost-efficient strategies can seek a higher yield while managing quality and liquidity characteristics in attempt to mitigate risk.

From recovery to expansion

In 2022, we expect the market narrative to transition from the “shock and awe” of the pandemic to the traditional expansionary phase of the business cycle. In this stage, bond investors benefit far less from owning generic market risk as central banks move toward the exits. A much more targeted approach focused on improving corporate and consumer balance sheets should lead to better outcomes in 2022.

Source: https://www.columbiathreadneedleus.com/blog/gain-clarity-in-2022-fixed-income-outlook