Schwab: Geopolitics-Examining The Top Five Risks

May 15, 2019

Key Points

- Recent developments have caused markets to focus on geopolitical risk, with more to come in the month of May.

- Geopolitical threats include renewed trade tensions, North Korean missile launches, Iran abandoning the nuclear deal, instability in Venezuela, and the European parliamentary elections.

- With global stocks vulnerable to a pullback, it is fortunate for investors that the trend in the degree to which the world’s stock markets move in sync with each other has been trending lower—enhancing the potential risk-reducing benefits of diversification.

Geopolitical risk has recently returned to the markets in the following five ways:

- renewed trade tensions between the U.S. and China and the looming possibility of auto tariffs impacting Europe and Japan

- new missile launches by North Korea

- the U.S. intensifying sanctions on Iran and deploying a carrier strike group to the Middle East

- an increasingly unstable situation in Venezuela

- the fragmentation that may result from the upcoming European parliamentary elections.

There are key geopolitical events on the calendar in the weeks ahead.

We will briefly examine each of these five geopolitical risks and their potential market impacts.

1(a). U.S.-China tariffs

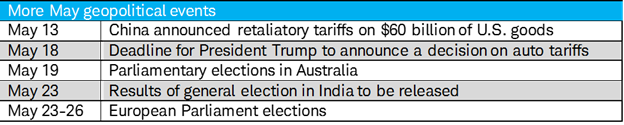

On May 10, the U.S. raised tariffs on $200 billion of Chinese made goods (with additional tariffs on about $325 billion potentially in the pipeline for later this summer). China pledged to respond in kind and has already announced tariff hikes on $60 billion of U.S. imports.

Despite the delay and tariff increase, it is still possible that talks may resume and a trade agreement may still be ready for signing at the G20 summit in Japan on June 28. Although first quarter economic growth in both the U.S. and China exceeded expectations and may have emboldened both sides to hold out on key concessions, growth may soften in the second quarter. The talks have been challenged by demands to enshrine changes into Chinese law and by efforts to create enforcement mechanisms. Yet, China has already publicly agreed to many U.S. priorities for a trade deal, including prohibitions on currency manipulation, allowing broader market access by foreign companies, implementing tougher protection of intellectual property rights and seeking more balanced trade. Many of these were outlined in a major speech by President Xi in April, as reported by Reuters.

A failure or lengthy delay to a trade deal would come at a bad time for the world economy. Global manufacturing activity is in the longest slump in the more than 20 year history of the global purchasing managers’ index. Stock markets remain very sensitive to trade issues, due in part to the larger representation of international exposure in corporate earnings than in the overall economy.

1(b). Auto tariffs

The trade deal with China was regarded as a sign of broader improvement in global trade relations. The May 18 deadline approaches for President Trump to announce a decision on auto tariffs impacting both Europe and Japan. Deterioration in the tone on trade risks escalating both investor concerns over tariffs as well as potential business disruptions.

2. North Korea

Demonstrating its frustration over stalled negotiations with the U.S., North Korea returned to missile testing last week. This was the first missile launch since late 2017, before President Trump began meeting with North Korean leader Kim Jong Un. However, these tests appear to have been short-range missiles rather than the long and intercontinental-range missiles North Korea agreed to stop testing. If the two sides do not resume contact and move toward some negotiations, North Korea may step up its efforts to grab attention, contributing to market volatility.

3. Iran

In early May, the U.S. declined to extend wavers to Iran’s oil customers to continue to make purchases. In response, Iran announced it would abandon commitments made under the nuclear deal. The U.S. intends to increase the economic pressure on Iran to force new nuclear negotiations. The chances of a military conflict have increased. Last week, the U.S. deployed a carrier strike group to the Middle East as a show of force. Iran stepped up nuclear-related activity and escalated movements by Iranian-backed forces posing a threat to U.S. and allied forces. In the past, heightened potential for conflict in the Middle East often impacted global stock markets through higher oil prices due to the risk posed to supply disruptions.

4. Venezuela

After the failure of an attempted coup, the government is cracking down and arresting those who supported the uprising, including high-level members of the military and legislature. Any move by the Maduro government to arrest opposition leader Guaido, currently recognized by the U.S. as the legitimate President of Venezuela, may cause the market to consider the possibility the U.S. may seek to remove Maduro through military force. Historically, global stock markets have tended to decline more deeply and for longer periods when associated with U.S. regime change operations compared with limited military strikes.

5. Elections

Although Australia and India are among the nations holding domestically significant elections in the coming weeks, it is the European Union parliament elections that hold the most potential to move the global markets. Pro-E.U. parties are expected to retain control of the E.U. Parliament. However, Euro-skeptic parties are likely to win more seats, resulting in a more fragmented legislature, potentially leading to a slower and more complex policymaking process as the risk of recession rises. The electoral outcomes could even affect the national governments of key E.U. countries: France, Italy, Germany, and the United Kingdom.

- In France, Macron’s low popularity in France could result in a poor showing by his En Marche party, potentially compromising his plans for fiscal stimulus in the form of tax cuts and spending hikes.

- In Italy, if the League party does well it may pull out of the coalition government with the Five-Star Movement and force an early general election, potentially renewing market concerns over Italy’s fiscal policy.

- In Germany, a poor showing by the Christian Democratic Union could prompt Chancellor Merkel to exit early and might even prompt a split in the coalition government with the Social Democratic Party backing out to improve their popularity. This may result in a minority government that would struggle to get things done, leaving Europe effectively leaderless.

- In the United Kingdom, the Brexit party may win the majority of seats, potentially sending a message that the U.K. wants a hard Brexit from the European Union in October. It may also strengthen the hand of those calling for Prime Minister May to step down in favor of a Brexit hard-liner.

The European parliamentary vote will add to the uncertainty over the future of the region and the direction of domestic policies. Both could weigh on stock markets.

What to do: Diversify the risk

Geopolitical risk is ever present, but developments cause it to affect the markets from time to time. In general, these threats tend to weigh on global stocks broadly rather than targeting only specific sectors or countries.

With global stocks vulnerable to a pullback, it is fortunate for investors that the trend in the degree to which the world’s stock markets move in sync with each other has generally been trending lower. The lower correlation between markets enhances the potential risk-reducing benefits of diversification (for more read our recent article Diversification: Back After 20 Years).

Source: Charles Schwab, various governmental organizations.