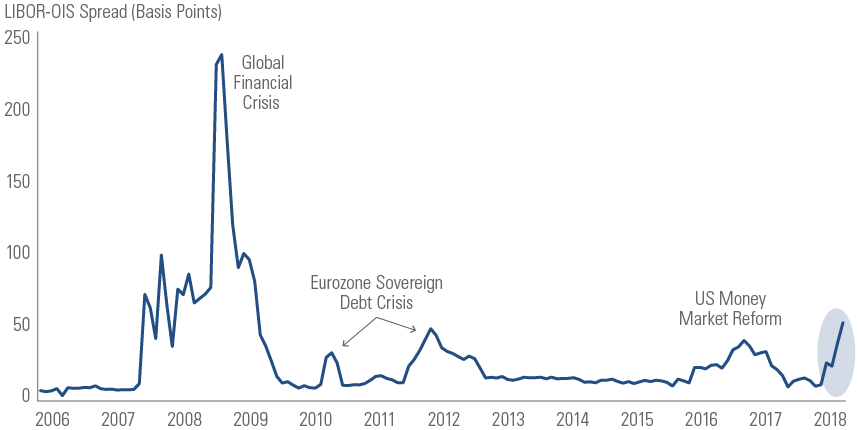

- Short-term interest rate markets have attracted considerable attention in the bond market recently, primarily due to a sharp rise in the London Interbank Offered Rate (LIBOR) relative to a measure of overnight interest rates known as overnight index swaps (OIS).

- Historically, market participants have watched the LIBOR-OIS spread for signs of stress in the financial system, but we believe other factors are currently driving this spread.

- We attribute the spike in spread to three factors: increased Treasury supply, repatriation and the “BEAT” Tax.

Wondering what’s happening in Short Term Rates?

April 5, 2018

Goldman Notes What’s Happening in Short-Term Rates:

FAQ: What’s Happening in Short-Term Rates

Overview

What is the LIBOR-OIS Spread and its market implications?

LIBOR and OIS are bellwether indicators of short-term borrowing costs. The LIBOR rate indicates the average cost a bank would pay to borrow from another bank in the London interbank market. Interbank loans are rare today because bank regulations penalize short-term lending and borrowing, but the three-month LIBOR rate remains a key benchmark for floating rates. OIS is a swap rate tied to the Federal Funds rate managed by the Federal Reserve.

While a rising LIBOR-OIS spread can indicate systemic concerns, it can also reflect more benign supply and demand factors. This was the case in 2016 when US money market reform reduced demand for prime money market funds, which invest in short-term corporate debt as well as government securities. As investors exited prime funds, demand for short-term corporate debt such as commercial paper declined, which put upward pressure on LIBOR.

What’s driving the spike in the LIBOR-OIS spread this year?

We believe three factors have contributed to oversupply in short-term debt markets and driven underperformance in LIBOR versus OIS:

Increased Treasury supply: In February 2018, Congress passed the Bipartisan Budget Act, which increases deficit spending and suspends the statutory limit on US government borrowing (the “debt ceiling”) until March 2019. With the debt ceiling suspended, Treasury bill issuance has soared as deficit spending increases and the US Treasury rebuilds its cash balances. We believe this extra supply has put upward pressure on interest rates across the short-term bond markets, including Treasury bill rates as well as LIBOR.

Repatriation: US multinational companies—particularly those in the technology and pharmaceutical sectors—have been holding foreign profits overseas rather than face the tax consequences of repatriating those profits back into the US. Much of that “trapped cash” was invested in short-term, dollar-denominated corporate bonds. In December 2017, the US passed tax reform that incentivizes companies to repatriate foreign profits. We believe this has reduced buying and increased selling of short-term corporate debt. As a result, spreads on short-term corporate debt have widened sharply in 2018.

The “BEAT” Tax: As part of the December 2017 tax reform, the US enacted a measure to reduce the erosion of the US tax base—the base erosion and anti-abuse tax (BEAT). Essentially, this tax makes it more difficult for multinationals to move cash between US and non-US entities. We think this has created a situation where non-US banks now need to source US dollar funding in the US (as opposed to using non-US deposits that were then converted to US dollars via the cross-currency basis swap market). In other words, a Japanese bank that previously used deposits from Japanese investors to fund US operations is now more likely to issue debt in US dollars to fund its US operations. We think this is yet another source of increased supply in short-term markets